Signs of Steady Progress: Spain’s Property Market in Q3 2024

The Spanish property market—long a source of fascination for sun-seekers, investors, and speculators—has reached another pivotal moment. The Q3 2024 data reveals a narrative of adjustment rather than decline, stability rather than stagnation. And while the sceptics- may clutch their pearls at the headline figure—a 12% drop in transactions compared to Q3 2023—closer inspection reveals a market in the process of finding its equilibrium.

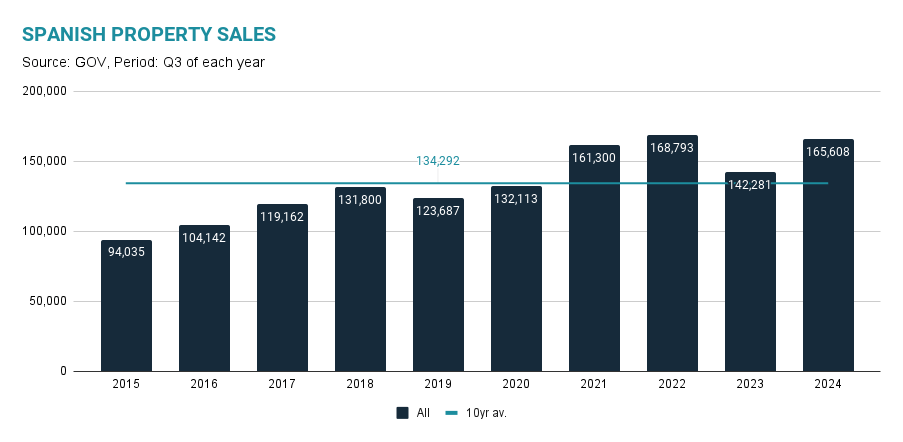

In raw numbers, 129,673 homes were sold in Q3, a decrease from the same quarter last year. Yet perspective is everything. These sales took place in a market facing rising interest rates and inflationary pressures, both global in scope and hardly unique to Spain. Viewed in this context, the volume reflects not collapse, but resilience. Even in challenging conditions, the Spanish property market continues to attract buyers, both domestic and international, who understand its enduring value.

The Costa del Sol, one of Spain’s most iconic regions, saw 7,893 homes sold—a fall of 14%. Yet even this, upon reflection, can be seen as a kind of silver lining. What we observe here is not the frantic churn of speculative bubbles past but a measured cooling-off period, one that allows the market to refocus on sustainable growth. Prices in this region remain robust, a testament to its continued appeal among foreign buyers.

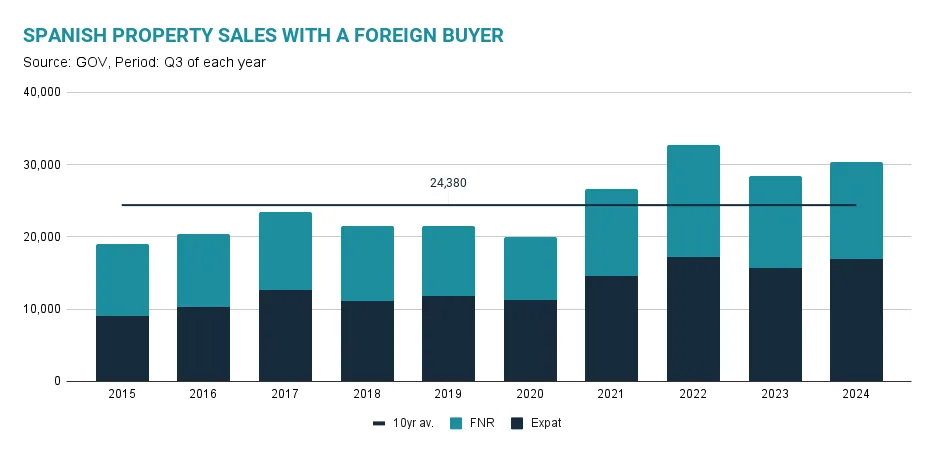

Indeed, the British are back, making up 9.6% of foreign sales—more than double the second-largest group of foreign buyers, the French (4.6%). Despite the bureaucratic quagmire of Brexit and its implications for second-home ownership, the UK’s enduring love affair with Spain remains alive and well. Meanwhile, foreign demand overall accounted for 15% of total sales, showcasing the country’s magnetic pull even amid global uncertainties.

A shift in strategy among developers has also played a crucial role. With only 17,671 new builds sold this quarter, down 4% year-on-year, developers have wisely embraced a more cautious approach. Gone are the days of unchecked over-construction; today’s focus is on quality over quantity. This strategy bodes well for future stability, aligning supply with demand and avoiding the pitfalls of oversaturation.

Domestically, affordability remains an issue, but progress is underway. Government programs targeting first-time buyers and modest wage increases have allowed more Spaniards to step onto the property ladder. Meanwhile, the existing homes market, with 111,953 sales, remains the backbone of the sector—a reflection of both practicality and opportunity in uncertain times.

One might be tempted to call this a market in crisis, but that would be a failure to appreciate the nuances at play. This is not the boom-and-bust cycle of old; it is a recalibration, a slow and steady march toward balance. The Spanish property market is evolving, shedding its reputation as a speculative playground and becoming something far more enduring: a place where people invest not just for profit, but for the promise of a better quality of life.

Spain continues to offer what so few markets can: a combination of economic opportunity, cultural richness, and lifestyle allure. For those who look beyond the surface and understand the cyclical nature of markets, Q3 2024 tells a story not of retreat but of resilience. This is a market that endures—and with it, the dream of a sunlit home in Spain remains very much alive.